However, now that their cover is blown, why is Madoff (as well as Blagojevich) not arrested? Why aren't Madoff's accomplices (including his sons) arrested? Why is the firm in question still operating? These types of individuals, ones who have ruined the lives of countless people and institutions and in doing so undermined the very nation they live in, would have been arrested, tried and imprisoned in countries like China and Russia. Well, welcome to America, the nation of well spoken criminals posing as politicians and financiers, a nation where a teenager gets put into jail for having an ounce of marijuana in his pocket, while well dressed criminals that have ruined the lives of countless citizens get to maintain their lavish lifestyles...

Wake up you pathetic fools, look beyond the polished hype, this has been the real America, and it has been so for the longest time. Perhaps now you may begin to realize why I have been saying that our corrupt politicians in places like the former Soviet Union are nothing compared to these sophisticated criminals?! Who the fuck gave these professional criminals the moral right to judge other nations?

Nevertheless, Armenians riot, the Chinese riot, the French riot, Russians riot, Greeks riot... The real question is - why aren't Americans rioting in the millions over all these serious criminal activities, political murders, scandals and looting? Where is the anger in America? Why aren't concerned patriots attempting an insurrection? In this once called "land of the free and the home of the brave", who's looking out for the people?

I see a shit load of Chinese made American flags flying everywhere. But I ask - where is the real patriotism within Americans today?

Arevordi

************************

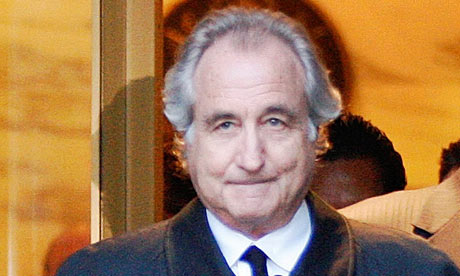

The secret life of Bernard Madoff unraveled as he stood in his upper East Side apartment in pale blue bathrobe and slippers, facing two FBI agents. "We're here to find out if there's an innocent explanation," Special Agent Theodore Cacioppi told him at the Thursday morning encounter. "There is no innocent explanation," Madoff replied. Within hours, investors who had trusted the 70-year-old Madoff for years - including the owner of the New York Mets - were reeling at charges that one of the most trusted names on Wall Street was a full-time fraud. Manhattan federal prosecutors disclosed a long-running scheme that may have resulted in $50 billion in losses - perhaps the biggest scam in Wall Street history. The one-time Nasdaq chairman, investigators charged, operated a classic Ponzi scheme, paying off early investors with funds from subsequent clients to keep the illusion of profit alive.

He tallied his deals in secret books locked in a filing cabinet a floor away from Madoff Securities' main offices, they said. His victims included Fred Wilpon and Saul Katz, co-owners of the Mets, who Friday acknowledged that their Sterling Equities had invested an unknown amount with Madoff. Spokesman Richard Auletta insisted Madoff's arrest "does not affect the day-to-day operations and long-term plans of the Mets organization and Citi Field." Wilpon even trusted Madoff to invest hundreds of thousands of dollars from family charities, documents show. In May, Madoff's wife, Marion, joined Wilpon's wife, Judy, to raise money for the United Jewish Association Federation in a charity bridge tournament. Since its founding in 1960, Madoff Securities won wealthy clients like the Wilpons by delivering steady profits through markets both bull and bear.

In January, the firm claimed Madoff's investment advisory business managed $17.1 billion for 11 to 25 clients. Madoff Securities boasted of an "unblemished record of value, fair-dealing and high ethical standards." Last week, the truth began to emerge as investors, spooked by the battered economy, decided to pull out their money. Madoff told an employee clients wanted $7 billion in redemptions, court papers state. He was "struggling" to get it, he said.

By Tuesday, Madoff announced he wanted to distribute employee bonuses, two months ahead of time. A suspicious senior employee said Madoff was "under great stress." On Wednesday, employees challenged Madoff's claim the firm recently made profits. He declared he couldn't speak of the situation at the office because he "wasn't sure he would be able to hold it together." They went to his E. 64th St. apartment, where he revealed his business was a fraud, that he was "finished," that he owned "absolutely nothing." Shocked employees, including his sons Andrew and Mark, called the Securities and Exchange Commission, which told the FBI. When the agents showed up at his apartment, Madoff admitted he'd "paid investors with money that wasn't there," was "broke" and knew "it could not go on."

Friday, angry investors crowded a Manhattan federal courtroom hoping to find out if the SEC would come to their rescue. Manhattan Federal Judge Louis Stanton issued an order freezing Madoff's assets, as well as those of his firm, and named lawyer Lee Richard to oversee the business. The hearing was canceled, leaving investors bewildered. "The one thing my father always told me was, 'Never sell your Madoff,'" said a Florida investor who believes he's out $3million he'd hoped to give to his children. "My only question is whether [the feds] will be able to salvage anything," he said. "My gut tells me no."

In related news:

- For almost 100 years, the US government has not felt constrained to match its expenditure with its revenue. This policy was given intellectual justification by the writings of John Maynard Keynes who argued in the 1930s that, during periods of slow economic growth, active and purposeful government policies would allow the economy to spend its way out of recession.[2] It was simply a matter of time before citizens aped the financial habits of their governments by living beyond their means.

- The Federal Reserve System (the Fed — created in 1913) has accommodated government's policy of spending to excess by inflating the money supply and keeping interest rates artificially low. Today's dollar will buy what in 1913 would cost less than a nickel. This easy-money policy has not only led to inflation but has resulted in investments taking place that would not be justified had the money supply been constrained, and had interest rates more clearly reflected economic reality.

- Since the 1960s, politicians parroting the suspect theories of Keynes have fed the public's naïve belief that government can provide ever-increasing living standards by means of its monetary and fiscal policies. Pulling a fiscal lever here and pushing a monetary button there meant that constraints on spending were old fashioned, and living standards would forever improve. The limitations imposed by the laws of economics had been repealed if you voted for politicians who promised to provide you with something for nothing. Fiscal prudence was simply a capitalist lie. It is against this long term, more philosophic backdrop, that the following, more immediate issues, assumed greater importance.

- Households collectively made little attempt to save for the future. The United States, in particular, borrowed from China, Japan, and Middle Eastern countries to finance its spending addictions. Financial responsibility was considered an old-fashioned, or even an irrelevant, virtue, and people were led to believe that government could, by waving its magic wand, provide improved housing without the pain of saving or foregoing immediate consumption.

- The acquisition of a house was viewed by many buyers not so much as having somewhere to live but as a painless way to make money. House prices, they naively believed, would always continue to increase in value while the relative burden of mortgages would continue to fall. Not only that, but as house values increased, a house could be used as collateral for a further loan. The financial equivalent of turning sea water into gold had been created. So long as house prices increased, borrowers were in financial heaven. When house prices fell, the earth opened up under the feet of lenders.

- # Government-sponsored entities like Fannie Mae and Freddie Mac subsidized mortgages for people who, under more-prudent rules of borrowing, would never have qualified for a loan from a conservative banking institution. Congressman Barney Frank in 2003 stated in a moment of candor, "I want to roll the dice a little bit more in this situation toward subsidized housing."[3] Well he certainly did, at the same time accepting with gratitude campaign contributions from Fannie and Freddie.

- The egalitarian policies of government through such legislation as the Community Reinvestment Act of 1977 "persuaded" lenders, Mafioso style, to lend to low-income borrowers, against their better judgment. Government lawyers made it clear that the consequences of failing to meet politically imposed targets and quotas could be dire.

- It was a matter of time before a substantial minority of borrowers could not or would not service their mortgages. Partly because astute people predicted this, well-known names in the financial world began to package, or sponsor, mortgage and other debts such as credit-card balances into what were called structured-investment vehicles (SIV), dubbed "financial weapons of mass destruction" by Warren Buffett. So complicated were the terms contained in such instruments that many legal minds and the credit-rating agencies were baffled as to exactly what they meant and where the ultimate risk lay. Banks and others could benefit by lending to people who could not afford to pay interest, far less capital, provided they were able to sell the SIVs to gullible investors. Money managers naively bought such investments for pension funds, money market funds, and (even more surprisingly) for their firms' own accounts. This was the primrose path to unlimited housing ownership, with no painful cash deposit, and no adverse consequences to the first lenders.

- So long as (a) the value of housing increased, (b) borrowers paid on time, and (c) confidence remained in the credibility of SIVs, everything was hunky-dory. Unfortunately, all three cratered about the same time; house values stagnated or fell as supply exceeded demand; when values stuttered, so did borrowers repayments, and confidence plunged. Borrowers, having promised to pay and having offered security for their promises, were failing to pay because their security had declined in value. They repudiated their debts, and the burden fell on hapless financial institutions. Populist politicians rarely blamed the borrowers, because there are so many of them and they vote; instead they blamed greedy capitalists, speculators, short sellers, anyone except the debtors, and the imprudent economic policies of the US government.

- As events began to unravel in mid-2008, well-established firms like Lehman Brothers, went to the wall. Others like Bear Stearns and Merrill Lynch were sold at knockdown prices. Yet others, like insurance giant AIG, were effectively nationalized.[4] Meanwhile, the stock-market value of banks and other financial institutions took a nosedive. For example, Citibank stock price fell by 79% between October 2008 and October 2009. The broader stock-market indices like the Dow Jones also plummeted by around 40%. The US government had no systematic policy, and rules were made up as more and more bad news emerged, especially about jobs. Citibank had a labor force of 375,000 in 2007; in November 2008, it was announced that 53,000 jobs would go by the first quarter of 2009. Senior government officials were like shipwrecked sailors (and were spending money like drunken sailors) paddling like mad but with little idea of where they were going, or why. The only consistent rule was that something had to be done, and the US government must be the action party.[5]

It is difficult not to recall the words of Herbert Spencer: "The ultimate result of shielding man from the effects of folly is to people the world with fools."

Government encouraged all of this by supporting affordable housing (which was politically correct) and accusing banks of redlining (failing to lend to poor and black people in the same proportion as they lent to the rich and white). When the borrower, already maxed out on his credit cards, predictably failed to make payments, the scale of the problems eventually became apparent to somnolent regulators and financial institutions. Confidence and trust evaporated, because no one knew which institutions held suspect securities, how much the losses were, and who was ultimately safe. A financial system built on debt and excessive leverage was a financial system built on sand.

The errors and fallacies that weave and surround this awful catalog of errors could have largely been avoided by paying attention to a single sentence written by Henry Hazlitt over 60 years ago:

The art of economics consists in looking not merely at the immediate but at the long effects of any act or policy; it consists in tracing the consequences of that policy not merely for one group but for all groups.

Source: http://mises.org/story/3263

No comments:

Post a Comment